Why Buying a Phone on EMI Is Actually a Bad Idea

Let me tell you about the day I walked into a Croma store with ₹8,000 in my pocket and walked out with a ₹52,000 iPhone on “zero-cost EMI.”

I felt like I’d cracked the system.

Twelve months later, I felt like the system had cracked me.

That phone — the one I convinced myself was a “smart financial decision” — ended up costing me way more than the sticker price. Not just in money, but in stress, locked-up credit, and a few lessons I wish someone had just told me upfront.

So let me be that person for you.

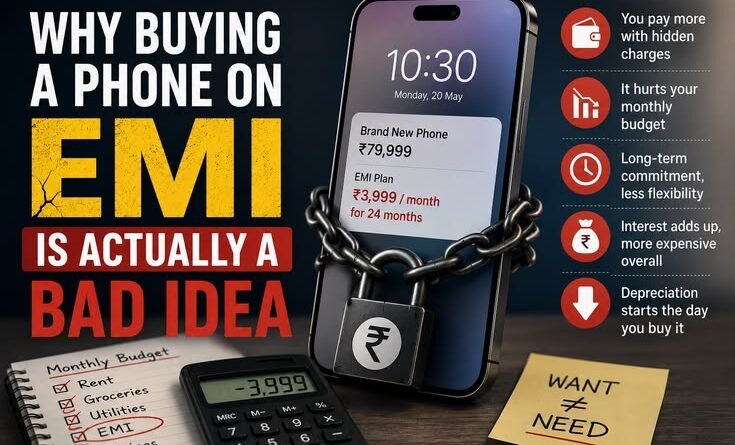

The “Zero-Cost EMI” Trap Nobody Talks About

The phrase “zero-cost EMI” is genius marketing. It sounds like you’re getting something for free. You’re not.

Here’s what actually happens: When you buy a phone on zero-cost EMI, the bank or the platform (could be Bajaj Finserv, HDFC, ICICI, or even Amazon’s own EMI) often charges the manufacturer or the retailer a fee. To recover that, the retailer typically marks up the phone price slightly, or removes any existing discount. You’re not getting the phone at MRP — you’re often losing out on the best deal available.

I figured this out when I saw the same iPhone I’d bought on EMI being sold for ₹4,500 less during a Flipkart sale. Cash buyers got the discount. I didn’t. I was locked in.

That’s the first sting.

The Real Cost Calculation Nobody Does at the Store

Pull out a calculator and actually do this math before your next EMI purchase.

Say you’re buying a phone for ₹40,000 on a 12-month EMI with a credit card that charges 1.5% per month on the outstanding balance. The total interest you’ll pay comes to roughly ₹3,900–₹4,200, depending on how the bank calculates it.

That’s not a small amount. That’s almost a budget phone.

Even on “no-cost” EMI, look at the processing fee. That innocent-looking ₹499–₹999 processing fee is your actual interest, just renamed. And it’s often non-refundable, even if you prepay the loan.

One more thing — if you pay via a debit card EMI (like the ones Flipkart pushes), they freeze the full amount in your bank account for the entire tenure. You “technically” have that money in your account, but you can’t touch it. It just sits there, doing nothing, while the bank is essentially borrowing your money for free. Wild, right?

What It Does to Your Credit Score

This is the part that surprises most people.

Every EMI you take on shows up as a “loan” on your CIBIL report. If you have 3–4 active EMIs — phone, laptop, maybe that air fryer you didn’t need — your credit utilization shoots up. Lenders looking at your profile see someone who’s perpetually borrowing.

This can hurt you when it actually matters — say, when you’re applying for a home loan or a car loan. A bank officer once told me (during my own home loan application) that even “small” EMIs significantly affect loan eligibility calculations.

Your ₹3,000/month phone EMI might literally reduce the home loan amount you qualify for. That’s not a hypothetical — that’s a real tradeoff.

The Upgrade Addiction Problem

Here’s something the phone industry absolutely loves: EMI makes you upgrade way more often than you should.

Think about it. When you buy a phone outright, you feel the pain of spending ₹45,000 all at once. That anchors you. You hold onto that phone longer, you protect it better, and you don’t go chasing the next model.

But when it’s ₹3,750/month? That doesn’t feel like anything. The new model drops six months later, you’re already halfway through your current EMI, and suddenly a salesperson is convincing you to “top up” your loan or take a new one.

I watched a friend cycle through three phones in two years this way. He was never actually without debt. He’d finish one EMI and immediately jump into another. When I asked him how much he’d spent on phones in those two years, he genuinely didn’t know. He’d never thought of it as one number.

It was over ₹1.3 lakh.

When It Genuinely Makes Sense (Being Fair Here)

Look, I’m not going to pretend there’s never a case for EMI. If you’re a freelancer or a content creator and your phone is literally your income-generating tool, then buying a high-end camera phone upfront might not be practical.

But even then — the right move is usually to save for 2–3 months and buy it outright, rather than committing to 12 months of payments.

The one scenario where EMI makes a tiny bit of sense: if you have a credit card with a genuine zero-cost EMI offer (no processing fee, no hidden markup, actual 0% interest), AND you have the full cash already sitting in a liquid mutual fund or a savings account earning decent returns. In that case, you’re essentially using the bank’s money while yours keeps earning interest.

But be honest — most people buying phones on EMI don’t have the cash already available. That’s the whole reason they’re doing EMI.

Common Mistakes People Make (That I Made Too)

Not reading the foreclosure terms. Most banks charge a foreclosure penalty if you want to pay off your EMI early — usually 2–5% of the remaining amount. I tried to close my EMI early and ended up paying ₹1,100 as a penalty. I didn’t read the fine print.

Assuming the insurance add-on is free. Retailers love bundling phone insurance or extended warranties into EMI plans and rolling it into the monthly amount. You’re paying for it. Always ask what the base phone price is, separately.

Buying on EMI because everyone else is. Social pressure is real. At my office, three colleagues were debating Samsung Galaxy S-series phones. Nobody wanted to say they were waiting to save up. I caved too. Don’t let that be you.

Ignoring alternatives. Refurbished phones from certified platforms like Cashify, Togofogo, or even Apple’s own certified refurbished store give you flagship-level hardware at 30–40% less. A refurbished iPhone 14 can feel just as good as a new one — and you can buy it outright without the EMI drama.

What I Do Now Instead

After my EMI lesson, I completely changed how I buy phones.

I set up a separate savings goal on my HDFC SmartWealth app (you can use any UPI or savings app — even a simple recurring deposit works). Every month, I auto-transfer ₹3,000 into it. After 12 months, I’ve got ₹36,000. That, plus whatever my old phone fetches on OLX or Cashify, usually covers most of a mid-range flagship.

No debt. No credit utilization hit. No stress when the bank sends an EMI reminder.

I also stopped chasing flagship phones altogether. The OnePlus Nord, Pixel 8a, and Nothing Phone line have genuinely made this easier. These phones at ₹25,000–₹35,000 are legitimately excellent — they’re not “budget compromises” anymore. You can buy them without feeling like you’re settling.

One More Thing About “Status”

I want to say this plainly because it’s something we don’t talk about enough.

A lot of phone EMIs are driven by status — the desire to have the latest iPhone or the foldable Galaxy at a party or a meeting. I get it. I’ve been there. But financing a status symbol is one of the most quietly damaging financial habits you can have.

The people who actually have money usually aren’t buying ₹1.5 lakh phones on EMI. They’re either buying it outright without blinking, or they’re using a mid-range phone and putting their money into things that grow.

You don’t owe anyone a flagship phone.

The Bottom Line

EMI feels like a shortcut. It’s actually a long road that costs more money, ties up your credit, and keeps you in a cycle of always owing someone something.

Save up. Buy outright. Or buy smart — refurbished, mid-range, or whatever fits your actual budget without a payment plan.

Your future self — the one applying for a home loan, or just trying to have some breathing room in their monthly budget — will genuinely thank you.

Got a different experience with EMIs? Or a trick that’s worked for you? Drop it below — I read all the comments.